%2520(1).webp)

Introduction

The Single Euro Payments Area (SEPA) represents a significant step in financial integration across Europe, standardizing euro-denominated bank transfers within the EU and EEA. Established to simplify cross-border payments, SEPA enables individuals and businesses to make cashless payments to anyone located within the area under uniform terms and conditions. This initiative, driven by the European Union, has greatly enhanced transactional efficiency, reducing costs and transfer times, thereby fostering a more cohesive economic environment across Europe. This article delves into SEPA's framework, its impact on European transactions, and its role in harmonizing the payment landscape.

History of SEPA

SEPA was officially launched by the European Payments Council in 2008, following the introduction of the euro. The aim was to create a unified payment area within Europe where consumers, businesses, and other economic actors could make and receive payments in euros under the same basic conditions, rights, and obligations, regardless of their location. SEPA covers not only the Eurozone countries but also extends to include other members of the EU and EEA, allowing for seamless euro transactions across national borders.

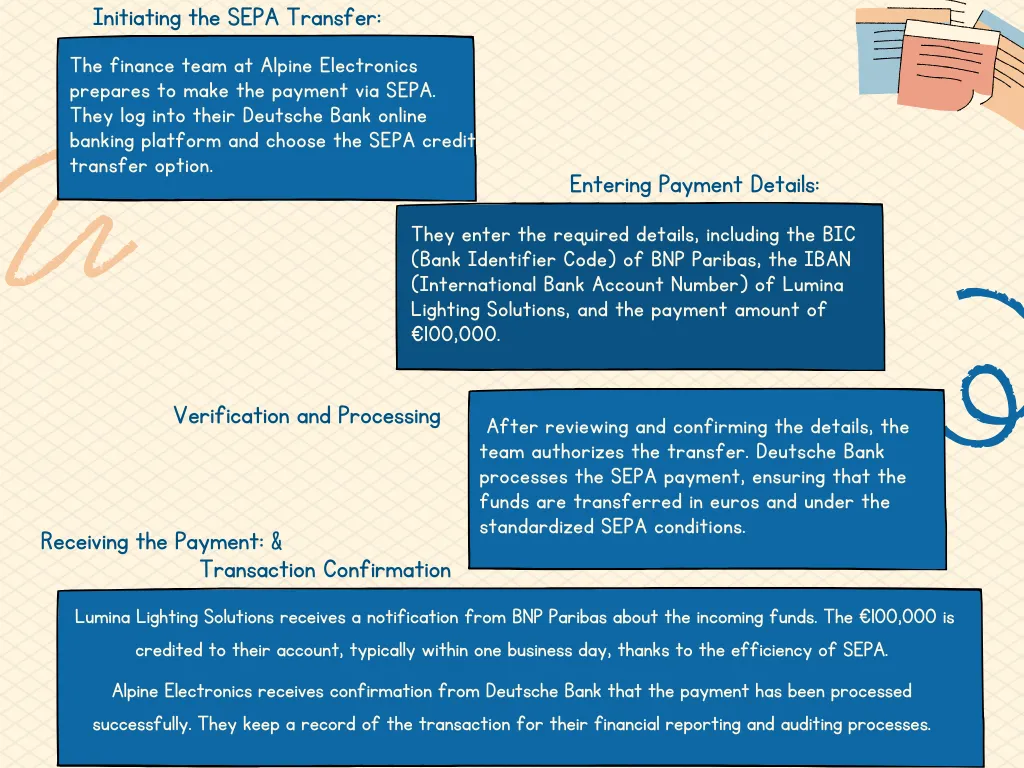

Business Scenario

'Alpine Electronics GmbH', a tech company based in Germany, needs to pay a supplier, 'Lumina Lighting Solutions', based in France, for a bulk order of electronic components. The payment amount is €100,000. Alpine Electronics banks with Deutsche Bank in Germany, while Lumina Lighting Solutions holds an account with BNP Paribas in France.

SEPA Transfer Process

While there are several advantages to the system, it's important to also recognize its limitations. Let's take a look at both the benefits and the challenges to fully understand the system's features.

Costs Involved in the Transfer Process

For businesses, the cost can vary depending on the bank and the specific business banking package. Some banks may charge a nominal fee per transaction, especially for SEPA credit transfers. However, these costs are typically less than those for non-SEPA international transfers, making SEPA a cost-effective option for businesses operating within its zone.

Timelines for the Transfer

SEPA credit transfers usually take one business day to be processed. This means that funds sent via SEPA are typically credited to the recipient's account the next working day after the transfer is initiated. SEPA direct debits have a different timeline, with pre-notification required at least 14 calendar days before the due date unless agreed otherwise between the payer and payee.

How Finofo Can Help?

Europe stands as a crucial hub for global businesses, but establishing a local entity or adapting your operations to European standards can be challenging due to stringent regulations. This may limit your ability to fully leverage SEPA's potential. However, there's no need to fret. Finofo offers a solution to this hurdle. By enabling you to open a local account, Finofo transforms your business into an effective local player in the European market. With this capability, you can utilize SEPA more efficiently, ensuring smooth transactions with your European customers and suppliers.

Curious to know the cost of sending supplier payments to Europe using local payment rails like SEPA through Finofo?

Check it out here – finofo.com/tools/send-money